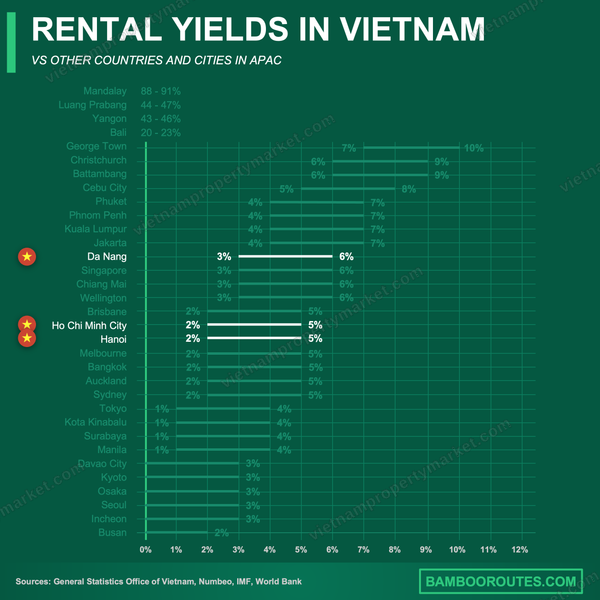

What is the average rental yield in Ho Chi Minh City?

Ho Chi Minh City's rental yields currently range from 3% to 7%, depending on property type and location, with studios and small condominiums delivering the highest returns at 5–7%. As of September 2025, the rapid rise in property prices has produced yield compression — but Ho Chi Minh City still outperforms other major Southeast Asian cities such as Bangkok and Jakarta.

District 2 and Binh Thanh are the strongest sub-markets in terms of yield and stability, and smaller units continue to outperform larger ones on rental returns.

| 부동산 유형 | 총 임대 수익률 — 인기 지역 — 평균 임대료 (USD/월) |

| 스튜디오/1베드룸 콘도 | 5–7% — 2군, 빈탄군 — $300–1,200 |

| 2–3베드룸 콘도 | 3–5% — 7군, 2군 — $700–1,700 |

| 타운하우스 | 4–6% — 7군, 투득시 — $1,500–2,000 |

| 빌라/주택 | 3–5% — 2군, 7군 — $1,100–4,500 |

| 단기 임대 | 8–12% — 1군, 2군 — 1박 평균 $46 |

What are the current rental yields by property type in HCMC?

As of September 2025, rental yields in Ho Chi Minh City vary widely depending on property type and location.

Condominiums achieve an average gross rental yield of around 3–6%, with sizable variation by floor area and location. Studios and 1-bedroom units consistently record yields of 5–7%, supported by strong demand from young professionals and foreign tenants.

Villas and townhouses show rental yields in the 3–7% range, but in major residential areas such as District 2, District 7 and Binh Thanh, established properties typically deliver stable yields of 3–5%. In some developing outer areas, high yields of 8–20% are quoted, but these fall into the high-risk speculative-investment category and warrant caution from ordinary investors.

Detached houses yield 3–5% in established residential neighborhoods. Townhouses typically achieve 4–6% in central areas, and sometimes reach the upper end of that range in outer districts.

How do rental yields differ by sub-market across Ho Chi Minh City?

'In Ho Chi Minh City, sub-market location has a significant impact on both property prices and rental yields.'

District 2 (particularly Thao Dien and Thu Thiem) sees sale prices of USD 3,200–6,500 per m² and rental yields of around 4–6%. This area is favored by foreign families and international professionals, so liquidity is high and demand is steady.

Phu My Hung in District 7 has sale prices of USD 2,800–4,500 per m² and rental yields of 3–5%. With international schools and well-developed infrastructure, it is popular with family tenants and foreign residents.

Thu Duc City (formerly District 9) offers relatively low entry costs at USD 1,800–3,200 per m², with rental yields of 3–6%. Demand is heavy from young professionals and students, but transaction liquidity is somewhat more limited than in the urban core.

Binh Thanh — home to Landmark 81 — sees prices in the USD 2,500–5,000 per m² range with rental yields of 4–7%. Excellent transport access and a diverse population (foreigners and local professionals) sustain strong rental demand.

In HCMC's real estate market, unit size shows an inverse correlation with rental yield.

Studios and one-bedroom apartments deliver the highest profitability, with gross rental yields of up to 7% in prime locations. These compact units are rated as the most cost-effective option for rental investors thanks to steady demand from solo professionals, foreign workers and students who prioritize location.

Two- to three-bedroom apartments offer mid-range rental yields of 3–5% and have the advantage of longer tenant retention. However, yields are somewhat lower than for smaller units. The main rental demand comes from small families and professional couples.

Large apartments, townhouses and villas typically show lower rental yields of 3–4%. This is driven by high acquisition costs and limited tenant demand: outside premium expatriate areas or specialized serviced-villa segments, the tenant pool is narrow and yields are compressed.

Nonetheless, mid-sized 2–3-bedroom apartments are rated as the 'sweet spot' for investors who want a balance between rental stability and yield. From a pure profitability standpoint, however, small units remain the most attractive.

How do purchase costs and taxes affect actual rental yields?

| 비용 항목 (Cost Category) | 비율 / 금액 (Rate / Amount) — 투자에 미치는 영향 (Impact on Investment) |

| 부가가치세 (VAT) | 부동산 가치의 5~10% — 상당한 초기 비용 |

| 등록세 / 인지세 (Registration / Stamp Duty) | 부동산 가치의 0.5% — 일회성 거래 비용 |

| 유지보수기금 (Maintenance Fund) | VAT 제외 가격의 2% — 아파트 인수 시 초기 비용 |

| 연간 관리비 (Annual Management Fees) | 월 ㎡당 8,000~120,000 VND — 지속적인 운영 비용 |

| 토지세 (Land Tax) | 연 0.03~0.15% — 연간 보유 비용 |

| 임대소득세 (Rental Income Tax) | 10% (부가세 5% + 개인소득세 5%) — 순임대수익 감소 |

| 중개 수수료 (Brokerage Fee) | 매매가의 약 2% — 거래 비용 |

Once all taxes, fees and operating costs are factored in, actual net rental yield is generally 1–1.5 percentage points lower than the gross figure. In practice, most apartments deliver net yields of around 2–5%, depending on location and management efficiency.

Mortgage rates have a major impact on leveraged investment returns in HCMC.

State-owned banks offer fixed rates of 5–7% during promotional periods, but these often switch to variable rates of 9.5–11.5% afterwards. For foreign investors, private-bank rates are higher still — typically over 10–12% — significantly increasing financing costs.

Short-term promotional rates over 3–5 years offer temporary relief, but the effective rate applied over the long term sharply reduces net yields. It is common for highly leveraged investors to see actual returns fall below 3% after debt servicing — a situation that is hard to improve unless property values rise quickly or rental income is unusually high.

For cash buyers, a gross rental yield of 3–7% delivers more attractive absolute returns, while leveraged investors must carefully calculate debt-servicing costs alongside expected rental income and capital-value appreciation.

In today's lending environment, properties combining conservative leverage with rental yields above 5% are best positioned to maintain positive cash flow even after financing costs.

In HCMC, short-term rentals and long-term rentals show a clear gap in profitability.

Airbnb-style short-term rentals generate an average of about VND 197 million (USD 7,000) per year, with an average daily rate of USD 46 and average occupancy of around 51%. Well-run listings in core central areas can hit gross rental yields of 8–12%, significantly outperforming traditional long-term rental yields.

However, short-term rentals are volatile, exposed to seasonal demand shifts (especially the December peak) and regulatory risk. Operating complexity and management costs are also high, so the actual net yield can fall well below the gross figure.

Long-term rentals, by contrast, deliver lower gross rental yields of 3–6% but are more stable thanks to high occupancy. Grade A serviced apartments, for example, maintain occupancy of around 85%, providing more predictable cash flow and a simpler tax structure.

Short-term rentals suit investors who actively manage operations and can absorb market volatility, while long-term rentals are more favorable for investors prioritizing stable, passive rental income.

As of September 2025, rents in HCMC differ significantly by property type and area.

Studio and one-bedroom condos rent for USD 600–1,200/month in Districts 1 and 2, USD 400–900 in District 7, and USD 300–600 in Binh Thanh. These ranges reflect location premium and the quality of the units.

Two- to three-bedroom condos in central areas rent for USD 700–1,700/month, with premium developments commanding higher rents. Family-sized units benefit from longer lease terms but see narrower demand compared with smaller units.

Townhouses in central areas typically rent for USD 1,500–2,000/month and are popular with families and small businesses seeking more space and privacy.

Detached houses and villas span the widest range, generally USD 1,100–3,000/month overall. Top-tier listings in Districts 1 and 2 reach USD 2,800–4,500/month, catering to upscale foreign families and executive demand.

Ho Chi Minh City's rental market is made up of multiple tenant types with varied backgrounds and needs.

Foreign professionals from Russia, Korea, China and Europe largely favor serviced apartments and condos in Districts 2, 7 and Binh Thanh, with some families choosing villas in the Thao Dien area.

University students prioritize proximity to campuses and rental affordability, mostly looking for studios and one-bedroom units in Binh Thanh and Thu Duc City.

Local professionals prefer 1- to 2-bedroom condos in Binh Thanh, Districts 1 and 4, or in emerging areas with strong transport access.

Foreign and local families need more space and rent large apartments, townhouses and villas, concentrated mainly in District 7 (Phu My Hung) and other areas near international schools.

Corporate tenants and multinationals often lease several units — or whole buildings — to operate executive accommodations.

Understanding tenant profiles helps investors pick the right property type and location to optimize occupancy and rental income.

Recent shifts in rental yields and rents

Ho Chi Minh City's rental market has experienced clear yield compression over the past five years.

Rental yields have steadily fallen from 4.02% in Q1 2023 → 3.83% in Q1 2024 → about 3.16% or lower in Q1 2025. The key driver is that property prices have risen much faster than rents.

Since 2020, rents have shown strong growth — new condos saw rents up 47% year-on-year in 2025. But even this rent growth has not kept pace with surging sale prices, so yields for new investors continue to be pressured.

Short-term rental revenue, by contrast, showed firmer momentum, up 4% year-on-year as of July 2025 — supported by the tourism recovery and rising leisure demand.

Yield compression reflects market maturation, growing investor interest and a shortage of quality supply in core locations — and it shows that new investors are entering the market while accepting lower returns.

Rental and yield outlook over the next 1, 5 and 10 years

Outlook for the next 1 year

Rental yields are expected to ease slightly or stay flat. Property prices will continue to rise, while rents are forecast to climb 5–7% citywide — underpinned by strong demand and a shortage of supply.

Outlook for the next 5 years

Demand is expected to keep growing, but yield compression is likely to continue. Yield improvement will be limited unless rents clearly outpace sale-price growth.

Districts 2 and 7 and the Thu Duc growth corridor in particular are expected to lead new development and investment flows.

Outlook for the next 10 years

Metro openings, the development of new CBDs and continued international-capital inflows will reinforce Ho Chi Minh City's competitiveness, and the city is likely to keep its yield edge over Bangkok (3–4.5%) and Jakarta (2.5–3.5%).

Long-term rent growth, however, will depend heavily on policy changes, tax adjustments and macroeconomic health.

Over the long run, investors who get in early in areas with improving transport infrastructure, growing foreign communities and emerging development axes will reap the greatest rewards.